Understanding Bitcoin through an ESG lens

George Frith is part of Superscript’s digital asset team and specialises in the digital asset ecosystem, covering everything crypto and web3. He previously spent six years underwriting property business for a well-known Lloyd’s syndicate, developing new product offerings and gaining a strong understanding of risk management principles.

Bitcoin, the 2009 creation of the pseudonymous Satoshi Nakamoto, was the first cryptocurrency to gain mass adoption. You’ve probably heard of it, you may even own some, but how much do you really know?

Michael Saylor is perhaps the biggest of what have become known as the ‘Bitcoin bulls’. Indeed, his company, Microstrategy, currently holds 124,391 bitcoins on their balance sheet at a cost basis of $3.75bn. Saylor remarks that it’s impossible to truly understand the Bitcoin network until you’ve put at least 100 hours of study in, a sentiment that I’d agree with. As you go ‘down the rabbit hole’ of Bitcoin, you unearth layer upon layer of ever-increasing complexity. However, I would question, do you really need to know what the mempool is to make a sound judgement on whether Bitcoin serves as a net good or bad for society?

What is Bitcoin? An overview for the uninitiated

Let’s begin with the 10,000ft view. The first thing to note is that ‘Bitcoin’ can refer to two distinct entities. Bitcoin the network:

- Is the first decentralised, peer-peer network that irreversibly stores transactions on the blockchain

- Allows two parties to send economic value to one another without having to use a trusted third party like a bank who will often take a fee for their work

Meanwhile, bitcoin the currency (with a lower case ‘b’) is:

- The unit of account used for transactions on the network

- Where the economic value is stored

- Sometimes referred to as ‘digital gold’ because of its store of value properties

A limited supply of 21 million bitcoins was created and a deflationary supply schedule set in motion which halves roughly every 4 years.

Others call bitcoin ‘digital energy’ because of the way bitcoin is created, using a proof-of-work consensus mechanism where energy is expended to solve cryptographic puzzles to mine new bitcoins and secure the network.

Bitcoin and ESG

In this article I want to look at Bitcoin through an environmental, social and governance (ESG) lens. In today’s climate of increased environmental consciousness, large corporations are falling over themselves to prove their green credentials, often facing accusations of ‘greenwashing’ as a result. As Bitcoin scales and becomes a major cog in the global financial system, so do the warnings from some incumbents regarding Bitcoin’s danger to the environment. But do these warnings carry any merit, or are they attempts to slow down mass adoption as a means of protectionism?

If we look back through history, we find it littered with incumbents trying to prevent the new kid on the block taking their share away from them. Take Western Union’s infamous 1876 memo:

This 'telephone' has too many shortcomings to be seriously considered as a means of communication. The device is inherently of no value to us.

Indeed, when Western Union tried to take Graham Bell out of the market by suing him for patent violations, they lost. Think also of the various ‘Red Flag acts’ of the mid 1800s, requiring a man with a red flag to walk in front of any motorised vehicle to warn oncoming carriages of the motor vehicles presence. The President of the Michigan Saving Bank is said to have told Henry Ford “the horse is here to stay, but the automobile is only a novelty, a fad”.

A sure-fire way to slow adoption of a new technology is to tell the public it will harm them or their environment in some way. Remember how mobile phones were going to give us all cancer? If you look at the narrative around bitcoin and cryptocurrency in general we are often bombarded with how it’s used predominantly by criminals, whereas in reality just 0.15% of all transactions were thought to be illicit in 2021.

Similarly, we are told about how Bitcoin’s energy consumption is going to use all of the available power in the world. An article in 2017 by the World Economic Forum told us that by 2020 Bitcoin will consume more power than the world does today, a prophecy that did not materialise. It begs the question, how could such a reputable, incumbent organisation make such a wildly bad call? In my opinion, the answer is simply that poorly executed research failed to correctly understand how Bitcoin scales.

How the Bitcoin community chooses to respond to such claims will go a long way to determining the future perception of the technology amongst both the public and regulators. The Bitcoin Mining Council has done a good job highlighting the environmental credentials of the industry, as has Nic Carter - a partner at the blockchain VC fund, Castle Island Ventures and veteran defender of the technology.

The Environment

That Bitcoin consumes energy is, I contend, an obvious but unhelpful truism. Certainly, Bitcoin consumes a great deal of energy, as much as a country like Argentina. However, I argue that the notion that Bitcoin’s energy consumption makes up an unsustainably massive part of global energy consumption is false, as is the idea that Bitcoin is, in essence, ‘stealing’ energy from those that vitally need it.

The statistics around Bitcoin energy consumption

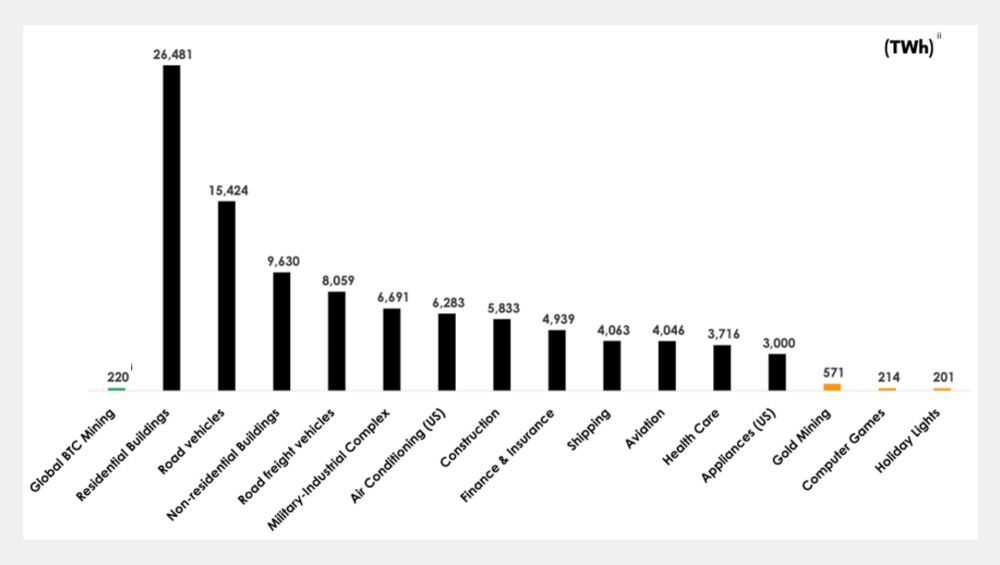

Let’s take a look at the numbers. According to research by Cambridge University the Bitcoin network’s power demand is 129.27 TWh at the time of writing. Compare this to global energy production of 167,716 TWh, and on this basis the Bitcoin network consumes just 0.08% of the world’s energy production.

To use a secondary data set, The Bitcoin Mining Council (who produce a quarterly report on the subject) reported in Q4 2021 that total energy production worldwide 154,750 TWh. Energy consumed by Bitcoin mining on the world’s electricity grid totalled 220 TWh, amounting to 0.14% of the world’s energy production. This in turn sustains a network with around $1trn total market capitalisation and over 100 million users. For context, 50,000 TWh of energy is lost annually due to inefficiencies in grid networks.

Given these figures, I would equate Bitcoins energy consumption to a rounding error, especially when compared to the attention it receives. The chart below featured in the same report really puts it into perspective.

Source: BMC Q4 Report

Why does Bitcoin consume energy?

At this point it’s worth pausing to consider why Bitcoin consumes energy at all? The main reason is that it acts as a means to secure the network from malicious attacks. In a system where there is no single authority controlling the network, what stops someone from gaming the system? Well ultimately, it’s that the economic incentive to do so is so penal it’s not worth doing. To attack the network one entity would have to control over 51% of the network, requiring a quite staggering investment to gain control over the hashing power to do so. The larger the network becomes the less likely this is to occur.

In reality, Bitcoin as a technology is entirely agnostic towards its energy input as long as it’s there to keep the specialised computers (ASIC’s) hashing. Whether the energy input is sustainable or not is down to the bitcoin miners and how they choose to source their energy inputs. Based on this logic, there is no technological reason why the Bitcoin network could not, or should not, run entirely on sustainable energy.

Bitcoin’s role in energy supply and demand

When we think about the energy grid, it’s important to remember the supply and demand dynamics. The grid providers are continually searching for an equilibrium between supply and demand. A good way to think of this is a tug of war between two teams, representing supply and demand. If both teams are equally balanced the grid runs smoothly, if the demand side suddenly adds four new team members the supply side will fall over. This is effectively what happened in Texas during winter storm Uri in early 2021.

As countries and states move towards net zero carbon emissions and more renewable energy sources, the supply element could become more unstable due to prevailing weather conditions. Bitcoin miners can help fix this by becoming a source of what is known as ‘interruptible load’. This means that they can switch their demand off at short notice. If we think back to the tug of war example, the miners would form part of the demand team and would let go of the rope when the four new participants join the tug of war, ensuring that the equilibrium of supply and demand remains.

Texas, with its large amounts of renewable energy has been a hotspot for miners. Wind and solar make up roughly 30% of the energy mix, with this expected to continue growing over the coming years. Following the energy crisis as a result of winter storm Uri last year, The Electricity Reliability Council of Texas (ERCOT) came in for significant criticism and has since been actively encouraging bitcoin miners to set up in the state. This may seem counterintuitive in a state that already has serious issues with disruptions in energy supply, but the miners can actually offer a number of benefits to the renewable energy credentials of the state:

- Bitcoin mining represents a source of so-called ‘interruptible load’

- Miners can go offline at short notice when there is a surge in demand on the grid

- Each individual computation is statistically independent of the previous one, so the process of mining can be stopped at any moment without a loss of progress

- Miners create a stable and flexible base load on the grid. Utilising otherwise wasted energy.

During periods of low demand Texas often has a surplus of energy, so much so that around 10% of the time ERCOT pays companies to take the energy off them.

Miners can create an additional revenue stream to help finance otherwise unattractive renewable energy projects. Wind or solar farms cannot easily store excess energy produced, so instead can sell otherwise wasted energy to miners allowing them to stay economically viable and encouraging more renewable capacity development.

Reduce reliance on fast start-up gas fired plants. During times of peak demand, the traditional response is to fire up combined cycle gas turbine plants (‘peakers’) that take roughly 45 minutes to an hour to get up to speed. Using these is ultimately more polluting than simply shutting off bitcoin miners, which can be achieved in around five minutes.

What becomes clear is the competitive advantage bitcoin miners hold over more traditional energy users that require an uninterrupted supply of energy at all times e.g. Amazon data centres, hospitals or even your refrigerator! That ‘interruptible load’ is vital to the continuation of the green revolution, so much so the International Energy agency has asked for 500GW of new demand response resources globally by 2030 to meet renewable energy targets. Ultimately, the Bitcoin network is increasing the elasticity of the energy supply by serving as a source of interruptible or controllable load.

In the current climate the attention tends to focus on the ‘E’ out of ESG, however the social and governance aspects should not be overlooked.

Social

Focusing on the ‘S’ in ESG, I’ll now explore the social benefits of Bitcoin. Advancements in technology have a reputation for displacing incumbent workers. Mark Andreessen’s famous ‘software is eating the world’ piece from way back in 2011 discussed the disruptive power of technology hailing the second coming of the tech revolution that was just re-igniting following the .com burst of the early 2000’s and the global financial crash of 2008/9. In the article, there’s a brief acknowledgement of the lack of sufficient education in the U.S required to participate in the growing tech ecosystem. I argue that what Adreessen failed to recognise is that the labour-light business models of these tech companies might be a factor in further exacerbating the wealth inequality we see in abundance globally today.

Technological advancements and labour

Let us take a step back and think about the advancement of technology over a longer timeframe. The advancement of technology during the agricultural revolution hollowed out traditional rural areas because there was no longer a need for the more expensive and less reliable ‘blue collar’ workers. I’m by no means advocating a return to the horse and plough to solve the skills gap. At heart I believe in harnessing technology, where at all possible, to increase efficiency and reduce human labour inputs. What I do strongly believe is that the playing field should be more even.

The average U.S student loan debt is $39,351, and an even higher £45,000 in the UK. This huge figure is prohibitive for many so they do not attend higher education and gain the necessary skills to participate in the ever growing tech economy as software continues to ‘eat the world’.

Bitcoin and social equity

So how does Bitcoin fit into this? Well there are currently no college degrees specifically relating to Bitcoin and one of the guiding principles of the crypto landscape, especially Bitcoin, is that everything is open source and available to all. If someone has the will and grit to educate themselves on this industry there is plentiful employment to be found.

Most of the world’s bitcoin mines are located in rural areas, helping to reverse the trend of young people leaving their local area due to a lack of financially rewarding employment. The Whinstone plant run by Riot Blockchain (located in Rockdale, Texas) employs over 200 local people with plans to expand further. In fact, bitcoin mining has the potential to empower local communities allowing them to become economically independent and generate prosperity.

Decentralised networks and access to investment opportunities

If we zoom out further still there are examples of bitcoin offering further social goods. One of the big attractions to a decentralised network is that it’s free for anyone to access, irrespective of geography, race, religion or class. As long as the user has an internet connection and a device that can connect to it they can access and purchase bitcoin if they so wish. Giving otherwise marginalised communities access to bitcoin and other blockchain related investments is a real levelling of the playing field.

It’s only in the past year or two that institutions have become involved in crypto in a big way. For perhaps the first time in a century, retail investors have been able to ‘front run’ institutions which made a welcome change to the current way of doing things. The current ‘accredited investor’ rules in the U.S and U.K prevent most retail investors getting involved in highly lucrative investments at an early stage.

In fact companies have been going public far later in their life cycles allowing private investors to extract far more value from them when they finally do. For example, Robin Hood (the well-known online trading firm) is down 69.4% from its initial share price of $38 in July 2021 to around $13 today. One can be fairly sure the early stage VC investor is not down 69.4%. Why should you only be allowed to participate in the best deals if you have an annual income of over $200,000 or a $1m net worth – we need to ask ourselves, does having that capital really qualify someone to make superior investment decisions than someone who doesn’t?

The case study of El Salvador

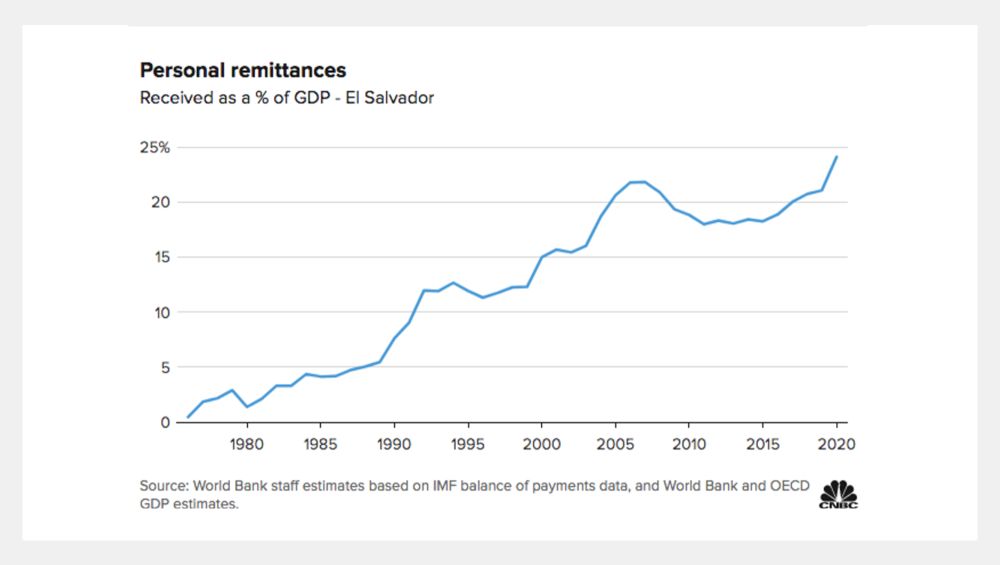

The current poster child for the adoption of bitcoin as legal tender is El Salvador. To some, this was a confusing decision because El Salvador doesn’t have a wildly volatile domestic currency. Instead, they are a dollar denominated nation. One of the reasons president Nayib Bukele regularly cites for doing so is the volume of remittance payments sent from abroad back to El Salvador on an annual basis. Over $6bn (or 25% of the country’s GDP) is remitted annually, from which wire transfer companies acting as intermediaries take their cut.

Using the Bitcoin lightning network, these fees will be vastly reduced allowing families to retain a far larger share of the wealth being sent home. All this in a country that is among the poorest in South America, where over 40% of the population live below the poverty line. Anything saved by using a different system has the potential to be a net benefit in the long run. Remittance fees charged by traditional wire transfer services can be up to more than 30% of the original transaction. For example, if an individual wanted to send $10 it would cost $3.24 or nearly 33%. For people on low incomes needing to send small payments back to El Salvador such fees are crippling.

Moreover, the time it takes to receive the funds via wire transfer can be up to three days. Using the lightning network the payment is almost instantaneous, or at most 10 minutes (the rough time taken for a new Bitcoin block to be added). If the move to adopt bitcoin as legal tender does nothing else, it introduces further competition to the legacy wire remittance companies. It should at least make them consider whether their fee structures are fair and reasonable.

Source: CNBC (World Bank estimates based on IMF balance of payments data, and World Bank and OECD GDP estimates)

Governance

I would argue that Bitcoin has a stunningly good record on governance as part of a decentralised, transparent, autonomous blockchain. No centralised entity has control over the network. Changes are made democratically and any changes to the rules have to be agreed upon by the three main stakeholder groups, known as community consensus. They are:

- The developer community

- The miners

- The Bitcoin node operators

Hence the rules are very hard to change. If they are changed, the update has been viewed as a benefit to the voting community.

Decentralised and democratic structure

This governance structure is poles apart from the centralised world we inhabit today where a few (generally unelected) individuals make policy decisions that affect all of us and our daily lives. Throughout history, central banks have devalued currencies around the world at will. One of the common theories for sky high equity and housing valuations is the devaluation of currencies vs. these ‘harder’ assets.

Recently South Africa, Turkey, Argentina, Venezuela have all experienced sudden negative currency fluctuations. Consider life in Turkey at the moment where President Erdogan has implemented currency controls to stop the population opting out of the Turkish Lira as it lost over 44% of its purchasing power vs. the US dollar over the past year. This can’t happen with Bitcoin because of its programmatic money supply and defined issuance schedule.

Ultimately, Bitcoin has no CEO, no board of directors, no HR department and no central office. It’s a network, not a company. By no means is it perfect and for many other blockchain technologies this entirely democratic model would be completely unfeasible. Yet when it comes to being a custodian over a ‘sound’ money or a store of value, I know which basket I’d rather put my eggs in, and it’s not one belonging to any central bank.

You may also like:

This content has been created for general information purposes and should not be taken as formal advice. Read our full disclaimer.

We've made buying insurance simple. Get started.

- 06 March 20245 minute read

Inspiring inclusion this International Women’s Day

Want to inspire inclusion in the lifecycle of your hiring and culture processes? We brought together two experts to give you their tip tips. Read on for more.

- 29 February 20244 minute read

What risks do gaming companies face?

Regulation changes, hacking, copyright claims, lawsuits… gaming companies sit in an ever-evolving space. Find out the top risks they face and how to tackle them.

- 13 February 20245 minute read

SaaS + AI = breaking boundaries (+ risk)

More and more, SaaS companies are utilising AI to stay one step ahead of the game. But what are the risks involved and how can they be mitigated? Read on to learn more.