Blockchain and tokens in the gaming industry

The gaming sector has come a long way since the first video game, Pong, was launched by Atari in 1972. Today’s online gaming market is much more sophisticated, much much bigger and ever growing in popularity.

Some milestones to note include the launch of Microsoft’s Xbox Live online gaming platform in 2001 which, for a monthly subscription fee, gave gamers access to multiplayer matchmaking; the release of World of Warcraft in 2004, selling over 14 million units and, finally, the game Final Fantasy, which – as of April 2021 – had over 22 million registered accounts, making it the most popular game in the world.

Redefining gaming

In recent years, the gaming industry has gone one step further, using blockchain technology and the creation of digital currencies/tokens to monetise these games and for the gamers themselves to become investors. And this trend is only expected to rise. According to Tech Jury: “Between 2017-2018, the gaming industry had a 13.3% compound annual growth rate to reach $137.9 billion. However, video games industry stats show that the industry hit the $152.1 billion mark in 2019, showing a CAGR of 9.6% from the previous year. Still, it’s expected to grow at a CAGR of 12% in the following years”.

A force to be reckoned with

Given there are 2.7 billion gamers globally, organisations have realised what a powerful and potentially influential cohort of people they are. So much so that the UN is looking at how to engage them in helping to tackle the challenges around climate change. Some, however, advise caution. This is not only because gaming firms have begun using Non-Fungible Tokens (NFTs) to boost their profits but also the use of NFTs could be damaging our planet. Susanne Köhler was quoted in The Verge saying: “NFT transactions may lead to increased greenhouse gas emissions, which will cause a rise in global temperatures and worsen climate change.”

A fruitful opportunity

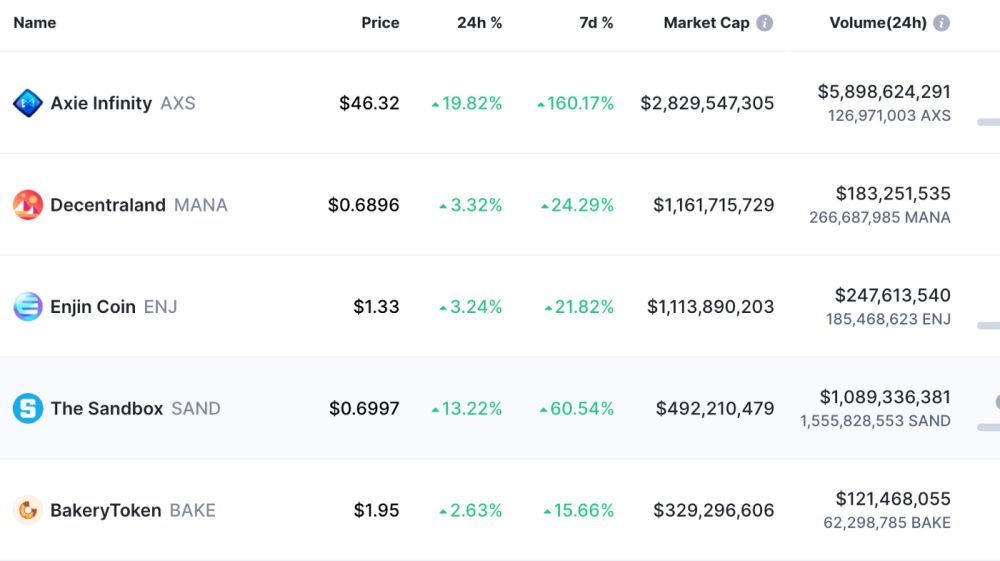

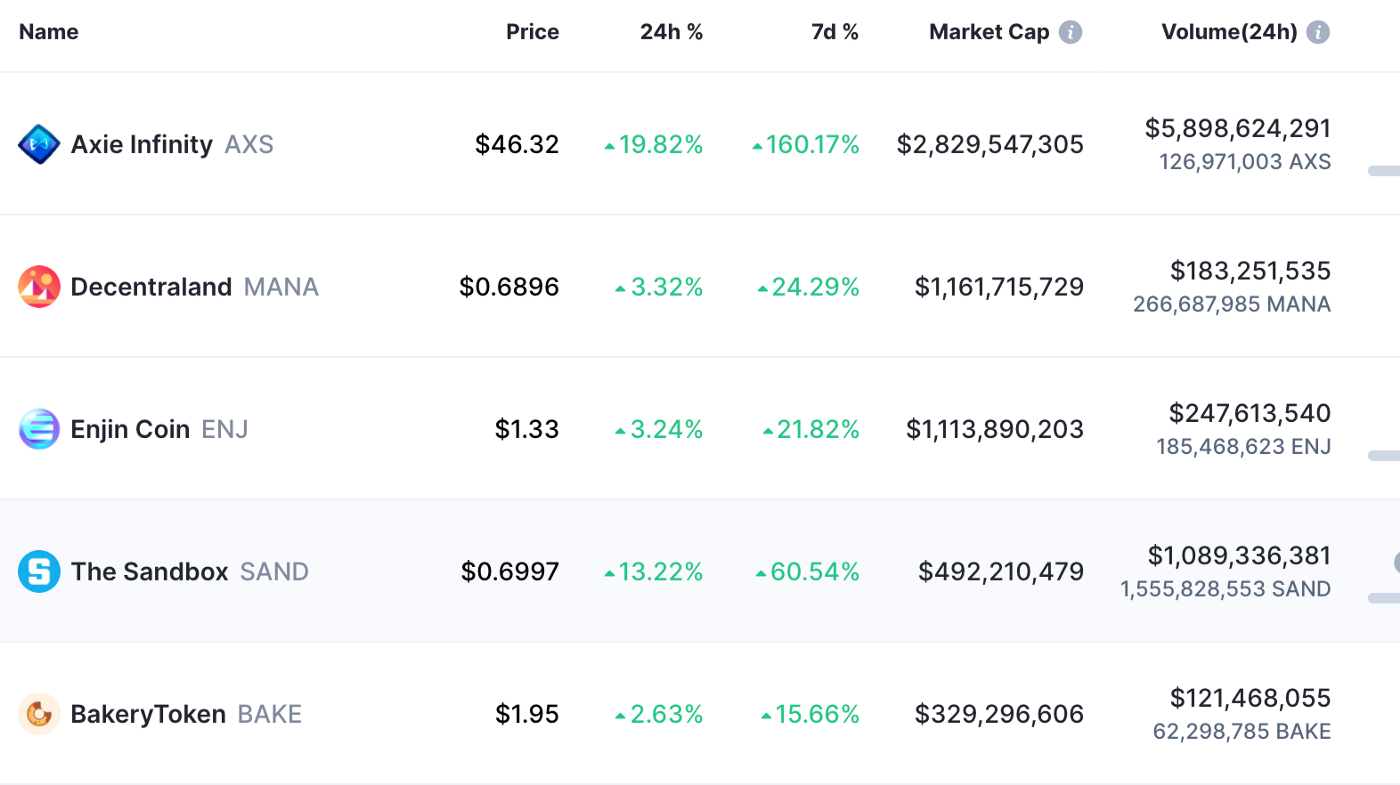

Despite its potential damage to the planet, the value of the five biggest tokens is impressive (all worth in excess of $300million). But the interest in these tokens, as defined by the turnover within a 24-hour period, is even more monumental. Two of the top five had a turnover valued at more than their market capitalisation, which illustrates just how big the demand from gamers is, not to mention the potential to make or lose money given the volatility in the price of some of these gaming tokens.

Organisations that run their own blockchains are targeting the gaming sector since, unsurprisingly, gamers generate plenty of activity. This means more transactions are required to be recorded on a blockchain resulting in more transaction fees. While these are tiny compared to Ethereum gas charges, millions of small charges can accumulate rapidly and be very profitable.

Source: Coinmarketcap

Polygon – a US-based, culture-focused gaming site – established Polygon Studios in June 2021, which will focus on creating Non-Fungible Tokens (NFTs) in the gaming market and has a $100m fund to help finance developers. One of the factors that affected the development in the blockchain gaming market has been the ‘gas’ fees, i.e. transaction fees when using blockchains such as Ethereum. However, Polygon has found a way around this by offering NFT platforms such as OpenSea, an NFT marketplace, to trade NFTs and not incur the uncertainty and potential large gas fees.

According to the US technology website, Venturebeat, “more than 60% of today’s NFT and blockchain-based web 3.0 games, including Decentraland, Sandbox, Somnium Space and Decentral Games have chosen Polygon’s Proof of Stake blockchain as the preferred scaling solution.”

But it’s not only Polygon that offers a Proof of Stake blockchain and low transaction fees, as well as helping gamers with funding. Chris Trew, founder and CEO of the Stratis Platform, is currently in discussions with a number of gaming firms looking to transition to the Stratis blockchain so as to utilise its low transaction fees and open architecture. Stratis, like Polygon, also offers funding to help develop businesses wishing to use the Stratis blockchain.

How else is blockchain changing gaming?

Devteam.com lists various ways blockchain technology is impacting the gaming industry:

- Blockchain prevents frauds

- Cryptocurrencies can make in-game purchases easier

- Blockchain provides a safe and secure environment for game developers and entrepreneurs

- Blockchain in gaming allows the buying and selling of in-game assets securely

- Blockchain in gaming enables interoperability players’ profiles

- Blockchain in gaming enables the projection of value on intangible assets

- Blockchain lets players securely store in-game assets

- Blockchain-based games allow players to truly own their in-game assets

- Blockchain allows players greater control over their favourite games

- Blockchain in gaming opens new territory for developers

- Blockchain allows players to collaborate with developers to improve a game

- Blockchain enables the creation of rarer in-game assets

It seems that gaming and the tokens that blockchains are able to create were almost made for each other as ways to encourage gamers to remain loyal and, increasingly, as a means for gamers to monetise their time. As the popularity of gaming continues to rise, undoubtedly so will be the various ways that tokens can be used.

You may also like:

We've made buying insurance simple. Get started.

- 03 March 20262 minute read

Superscript enters next phase of UK growth

Superscript opens a Glasgow hub, adds gig economy focus and strengthens leadership as it enters its next phase of UK growth.

- 05 December 20252 minute read

Superscript named winner of 2025 Digital Broker of the Year

Superscript wins big at the Insurance Times Awards 2025, taking home the award for Digital Broker of the Year. Learn more.

- 03 December 20253 minute read

Why insurance gives gaming studios an edge when pitching

Did you know? Insurance can give investors and publishers real confidence in your gaming studio — and help you close that next big deal.

{kind=link}